The Second China Shock is here

Tordoir and Setser's Policy Brief

An off-cycle post to respond to an extremely interesting Policy Brief released earlier today by CER on German industrial policy. Experimentally, I have not emailed it, in order to avoid spamming our readers. I would love to hear from you if that is a good approach for the future.

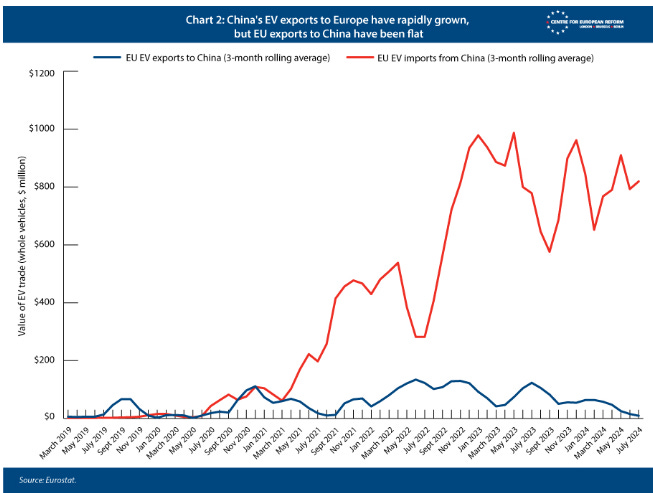

Sander Tordoir and Brad Setser just released a new CER policy brief. I strongly recommend that our European readers read it. It diagnoses well the grave challenge facing the German industry. German industrial production has declined for five years, China now exports 5 million more vehicles than it imports while German net exports have halved, and Chinese firms dominate emerging sectors like electric vehicles and solar panels. The second China shock is here, and it will be much worse for Europe than the first.

“The EU, with Germany at its industrial core, boasts 30 million manufacturing jobs: almost twice as many as the US had before the first China shock."

China’s manufacturing dominance is nearing unique levels in history:

"China's manufacturing surplus is now 10 per cent of its GDP – a staggering number... US trade surpluses in manufactured goods peaked at 6 per cent of American output early in World War I"

They are right to argue that this will force a dramatic restructuring of our industrial base. However the brief prescribes the wrong medicine.

Tordoir and Setser’s Proposals

Some of what Tordoir and Setser argue is uncontroversial. They are right that solid numbers on China’s trade surplus from the IMF are essential. I agree that Germany needs to rely on Chinese supply when efficient, it needs to stand with its allies, it needs to impose trade measures when and if China’s sectoral subsidies have distorted competition:

Where I part company with them is in their third and fourth recommendations. The third is their ”Buy European” provisions. These paragraphs give you a flavour of how crazy it can get :

One possible lever to enforce such criteria across the EU would be competition policy: the Commission’s enforcers could condition approval of national subsidy schemes on criteria that favour EU production, such as adherence to social standards, and exclude products associated with high emissions from long-distance transportation or coal-intensive production processes.

There may, however, be sectors like non-greentech machine-building or energy-intensive chemical production where existing EU regulations (like the NZIA) or product standards (such as the ESPR) provide insufficient hooks to do so. The EU could then pass new directives to co-ordinate subsidies. Unlike an EU regulation, an EU directive is a legislative act that sets out a goal all member-states must achieve, but allows them to decide how to transpose it into their national laws.

They enumerate a whole list of other complex, specific rules based on distance, social and environmental standards to make it de facto a rule to “buy European”. I would call this proposal (if the readers excuse the lack of decorum) a call for an increasing the “enshittification” of the Single Market- a continuing process of increasing regulatory complexity that is doing much to make our firms less competitive. Also, these clever rules will create all sorts of trouble with our friends in the US, Japan, Korea, Brazil, and South Africa. This is the path towards European decadence.

The fourth set of measures is doubling down on industrial policy by using the tariff revenue from the China tariffs towards an EU industrial policy fund. I think this gets it wrong by making it appear as if Germany (and Europe) has simply not attempted industrial policy. In fact the two examples where China is delivering its biggest blows are two where Europe, and Germany, did try.

In the early 2000s, Germany was first with solar subsidies that created the world's largest solar market.

“In 2010, Chinese production of solar Photovoltaic (PV) panels depended on imported German equipment. Now solar PV production globally relies on equipment imported from China."

These subsidies helped build a substantial European solar manufacturing industry. By 2012, European firms like Q-Cells, Solarworld, and Centrotherm were global leaders. Yet despite these advantages and continued trade protection, the European solar industry collapsed. Q-Cells went bankrupt in 2012, SolarWorld followed in 2017, and today China controls over 80% of every step in the solar supply chain and produces at half the cost of non-Chinese producers. This happened despite aggressive EU anti-dumping tariffs on Chinese panels in 2013 — exactly the kind of trade defense Tordoir and Setser now advocate.

European governments have poured billions into EV development and production: Germany provided €5 billion in EV purchase subsidies between 2016-2023; the big hope for EU batteries, Northvolt, just went bankrupt despite large EU and German subsidies.

Yet despite this massive support, Chinese EVs are now one generation ahead in technology — superior in range, charging speed, and software integration — and significantly cheaper to produce.

The issue isn't that Europe didn't try hard enough — it's that the fundamental conditions for successful industrial policy, as discussed previously in Silicon Continent, are absent in Europe's automotive sector:

Europe's auto industry is dominated by powerful legacy producers and unions who fiercely resist change. Unlike South Korea in the 1960s or China in the early 2000s, where there were few entrenched interests to oppose transformation, Europe's industrial system prioritizes protecting existing jobs and companies.

European industrial policy suffers from competing and often contradictory goals. Should it prioritize climate change (suggesting openness to Chinese EVs to accelerate adoption), protect jobs (favoring trade barriers), ensure technological sovereignty, or maintain competitiveness? This confusion has led to halfway measures - tariffs too low to protect the industry but high enough to slow the green transition.

The EV transition represents a classic case of disruptive innovation where incumbents struggle to adapt and survive. Just as Kodak couldn't adapt to digital photography, traditional automakers face fierce internal resistance to fully embracing electric vehicles. More worryingly, Europe has failed to produce new EV-native companies like Tesla, Rivian, or BYD.

Doubling down in these areas will mean throwing good money after bad. Europe has lost on wind, solar, and batteries. There are gigantic learning curves, and Chinese firms are way ahead. If we care about climate change, we fortunately have cheaper and cheaper solar, wind, and batteries. Europe's scarce resources should be used in the most productive way possible: areas where competitive advantage is still possible — complex industrial machinery, specialized chemicals, and high-end engineering where German firms still lead.

For policymakers: please stop regulating the industries that remain to death. We are here wringing our hands at how we lost solar panels while doing everything in our power to lose in AI. Europe needs to be the most innovative continent. Where are the new EV companies from Germany?

I don’t want to minimize the serious challenge the German industry faces. The potential loss of high-wage manufacturing jobs could devastate communities. But the solution isn't to repeat failed industrial policies with higher spending and stronger trade barriers.

Postcript: I wake up today to news in the Financial Times that European carmakers will have to pay billions in credits to Chinese electric vehicle manufacturers. While we are supposedly trying desperately to save our car industry, we are creating distorted fleet-wide quotas. This makes no sense. We should focus on removing harmful policies rather than dreaming up fancy new bureaucratic schemes.